January sales kicked off a solid month for retail with stores delivering their strongest growth in almost two years, albeit on a weak comparable.

According to the latest BRC-KPMG Retail Sales Monitor, UK Total retail sales increased by 2.6% year on year in January, against a growth of 1.2% in January 2024. This was above the 3-month average growth of 1.1% and above the 12-month average growth of 0.8%.

Food sales increased by 2.8% year on year in January, against a growth of 6.1% in January 2024. This was above the 3-month average growth of 2.3% and below the 12-month average growth of 3%.

Non-Food sales increased by 2.5% year on year in January, against a decline of 2.8% in January 2024. This was above the 3-month average growth of 0.2% and above the 12-month average decline of 1.1%.

In-Store Non-Food sales increased by 2.6% year on year in January, against a decline of 2% in January 2024. This was above the 3-month average decline of 0.7% and above the 12-month average decline of 1.7%.

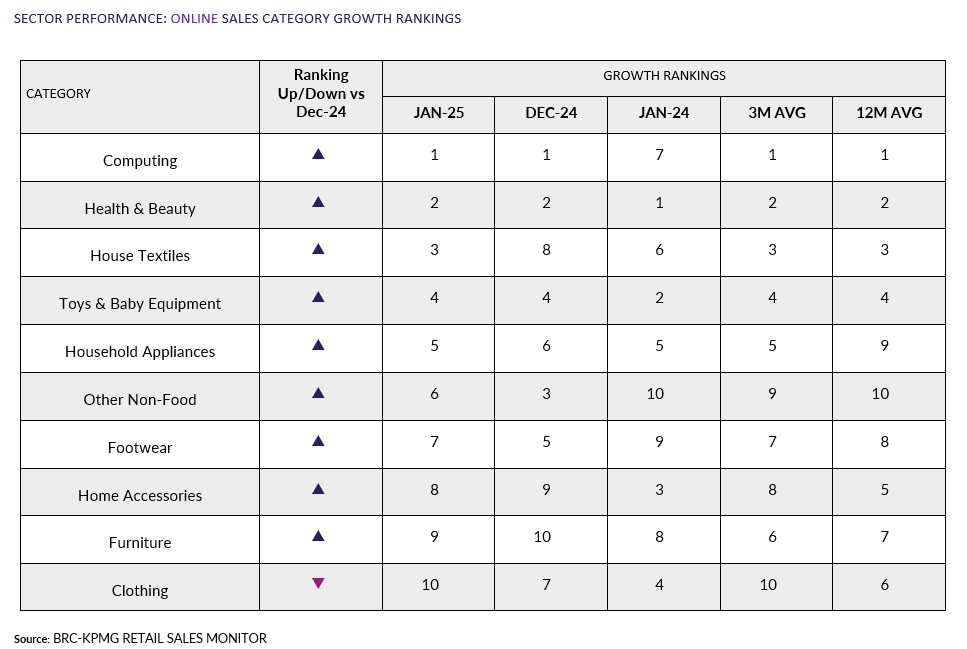

Online Non-Food sales increased by 2.2% year on year in January, against a decline of 4.2% in January 2024. This was above the 3-month average growth of 1.8% and above the 12-month average growth of 0.1%.

The online penetration rate (the proportion of Non-Food items bought online) decreased to 35.7% in January from 35.8% in January 2024. This was below the 12-month average of 36.7%.

Helen Dickinson OBE, Chief Executive of the British Retail Consortium, said: “Consumers headed to the shops to refresh their homes for the year ahead, taking advantage of big discounts on furniture, bedding and other home accessories. With growth across nearly all categories, only toys and baby equipment remained in decline. While the bouts of stormy weather put a temporary dampener on demand, sales growth held up well throughout the rest of the month. This was also helped by the earlier start of the reporting period, adding a few more post-Christmas shopping days into the mix.

“Whether this strong performance can hold out for the coming months is yet to be seen. Inflationary pressures are rising, compounded by £7bn of new costs facing retailers, including higher employer national insurance contributions, higher National Living Wage, and a new packaging levy. Many businesses will be left with little choice but to increase prices, and cut investment in jobs and stores. Government can mitigate this by ensuring its proposed business rates reforms do not result in any shop paying more in business rates.”

Linda Ellett, UK Head of Consumer, Retail & Leisure, KPMG, said: “2025 got off to a welcome start for retailers with much needed sales growth in January. But viewed over a three-month period that included Christmas and Black Friday, non-food sales have flatlined. Overall, the golden quarter failed to shine.

“The trading environment remains tough for retailers, with consumer demand still subdued and household essential bills still high. Business costs are also coming under pressure, with rising employment costs only increasing that in the coming months. Boardroom focus on costs and competitiveness is sharpening. Pricing adjustments, product launches, store closures, job losses, and increased automation and AI are all set to reshape the retail landscape in 2025.”